Are The Bond Vigilantes Looking for a Hanging?

Prior to 2000, it was common in the economic and investment literature to read about “bond vigilantes.”Credit for the term is generally given to investment guru Edward Yardeni.

James Carville, the snake-headed political advisor to the Clinton campaign in 1994, remarked that if there were such a thing as reincarnation, he would like come back as the bond market.

He was referring to the power the bond market has when it is allowed to operate, to inflict economic pain, and thereby reorder politics.

Both the theory and the actual operation of the bond market go something like this: As spending rises to unsustainable levels, bondholders demand higher interest rates for their risk of suffering a default by the issuer. Likewise, with inflation, often caused by excessive debts and spending, bondholders know they will be paid off at the end with money far less valuable than it was when they made their purchase, and they too will extract higher interest rates as compensation for inflation risk. In short, the market raises rates, with or without the FED.

Prior to 2000, bond vigilantes, while not doing a perfect job, helped keep government debt and deficits within reason, even when our politicians and institutions failed to do their job.The bond market and interest rates, sort of like the old gold standard that was abandoned, remained the only market-based external discipline in the system.

And like the discipline of the gold standard, central bankers needed to make an end run around the bond vigilantes just as they did with gold.

Under the Clinton White House and the Gingrich House of Representatives, helped by the pain inflicted by the bond vigilantes, the country enjoyed a short period of balanced or near-balanced budgets. The last one was in 2001.

Then the Federal Reserve embarked upon its binge of bailouts, utilizing policies perfected by the Bank of Japan, so-called Quantitative Easing. The tech crash in 1999-2000, then after the 9/11 attack and Mid-East wars, and then the 2008 financial panic, all seemed to demand the FED “do something” to stop the pain.

The FED accommodated both the Bush Administration and the Obama Administration, keeping the bond vigilantes at bay while spending and deficits rose and rose. Trump, while acting conservative in many ways, largely ignored debt and deficits as well.

While the Fed made a modest attempt to curtail QE and lift rates from zero in 2018, a stock market slump late in that year chased them off. They did not have the nerve to follow through.

We basically had 20 years of zero rates with expansive monetary and fiscal policy.

QE entails the Federal Reserve buying massive amounts of government debt (bonds and even mortgages). Where does the FED get the money to make these purchases? You guessed it, they printed it electronically.

The net effect was to sop up trillions in bonds that otherwise would have had to be dumped into the marketplace, which would have resulted in bond prices falling. By boosting demand for bonds artificially, they boosted bond prices artificially, and that artificially drove interests down to near zero and held them there for almost 20 years.

That has never occurred before in recorded economic history.

Zero rates and QE basically freed politicians from the last budgetary discipline that existed. The bond vigilantes could not do their job.

What would you expect politicians to do when freed from such discipline? Even with it abundantly clear that negative demographics and underfunded entitlement programs would increase deficits for years to come, new programs and new wars were always necessary.

But the money created by the FED stayed largely within the banks until Covid when the government began to just send out checks directly to the public. With the bond vigilantes essentially eliminated, politicians from both parties, but especially Democrats, went on a spending spree.

As they spent, there seemed to be no real inflation, in the classical sense. Some have argued it was because of productivity gains, globalization, aging of the population.Whatever it was, politicians and central bankers decided to stimulate the economy even during relative prosperity because they thought they could do it without inflationary consequences.

Covid gave them even greater opportunities and the adoption by Democrats of Modern Monetary Theory gave them intellectual cover. Now it seems the next emergency that must be funded by gigantic deficits is global warming.

It was all gain and no political pain.

But then things shifted. The money supply blew up 40% in 18 months, an unprecedented economic event, especially for the issuer of the global reserve currency. Inflation rose to near double-digit levels. Inflation rose sharply in most other parts of the world. Biden and the FED said it was “transitory”, but instead it has become entrenched. The FED reluctantly reversed course by raising interest rates and selling bonds from their balance sheet.

The US was not alone in this mess. Some foreign central banks were even more aggressive, some even purchasing assets like stocks and not limiting themselves to government bonds or government-guaranteed instruments. Globally speaking, debt has grown to about 350% of global GDP. Now, in less developed and developed economies, all countries are raising rates to one degree or another. It is starting to squeeze the global debt bubble.

As a result, bonds have had one of the worst years on record, and rates have not likely reached their peak. Home mortgage rates have virtually doubled. All manner of speculative activities, from SPACS and Cryptocurrencies to the stock market, have been plunging. Just in stocks alone, some $7.5 trillion have been lost so far this year. The bond vigilantes are riding again.

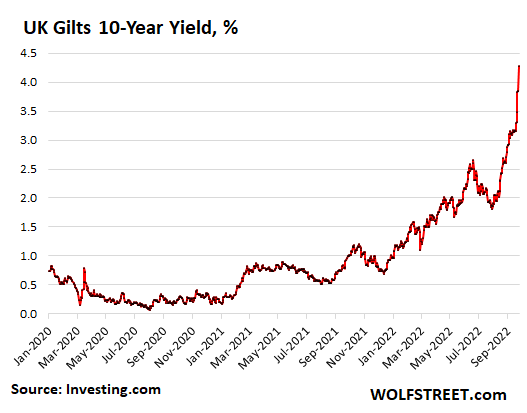

In some countries such as Great Britain, last week the bond market virtually collapsed and interest rates are soaring. The British Pound has fallen to a 40-year low. At least in the short term, the crisis reached a dangerous threshold, causing the Bank of England to pivot, that is to say, start QE again to save their bond market and the Pound. Thus, short-lived discipline was abandoned as the central bank pivoted back to inflationary easy money policies.

The quick reversal by the Bank of England was also prompted because pension funds that own bonds and bond derivatives are getting into trouble.

It also appears several large financial institutions, Deutsche Bank, Credit Suisse, and Softbank, are teetering with their stock prices plunging. The risk of financial contagion is rising.

The question is: are the bond vigilantes back or will the central banks once again “pivot” and try to neuter them again?

The US FED says it will persevere in raising rates until the inflation fever breaks. But their record both at prediction and in keeping their word is poor. The risk of policy error is high. The FED is raising rates into an early-stage recession.

It would seem that the bond vigilantes are back, at least for now, and they are looking to hang some people. Some of these will be politicians, who like Biden, will not be able to escape responsibility for the inflation and high-interest rates they have inflicted on the citizens.

But many innocents will be hurt. The young will not be able to afford a house, investors will lose trillions, and many will be forced to default. Some will lose their jobs.

One man’s debt is often another man’s asset. When you default on a loan, the person or entity that lent the money loses. One man reduces his debt, the other loses his shirt.

Once the bond vigilantes start to ride, the terror of default and failure will spread with their pounding hoofs.

If the central banks pivot too soon, they will lose credibility, and hope of controlling inflation will be lost.

Politicians and central bankers thought a perpetual motion government spending machine seemed to have been invented. In the end, it has put many nations into a real bind. Either run the risks of hyperinflation and avoid recession or allow interest rates to rise and cause a recession.

Remember, the recession is that part of the business cycle that corrects the excesses of the boom.

What makes it worse this time, is the same folks that brought you inflation now have a new scheme to make things worse.

In the midst of this painful, and dangerous process, they want to inflict on the world a new energy system, that is both expensive and unproven. Creating both a food and energy crisis, in the midst of a recession, will be something new again that we have not seen in any previous business cycle.

So, as your energy bills climb and the food budget is stretched, and your investment portfolio plunges; keep in mind the pain is all a product of bad policies, policies that could have been blocked in the narrowly divided US Senate. The only hope is to vote them out of office, the people who brought you these bad policies. If that can be done, the problems they created will remain but at least, they won’t get even worse.

The Senate is almost perfectly divided so the Senatorial races are key.

Mark Kelly could have been a hero to Arizona and the nation. He could have stopped most of the mad spending that forced the FED to accommodate them. True, Manchin and Sinema did cave in the end, but Mark Kelly has never lifted a rhetorical or voting finger to stop the financial madness. Had Manchin and Sinema just had another ally or two, they might have held.

But Mark Kelly was silent during the struggle, apparently too busy being Biden’s and Schumer’s poodle to care.

If we can’t find politicians with the gumption to control our finances and allow the private sector to produce energy, we will have to deal with the bond vigilantes. They will hang us all without mercy.

And that means people like Mark Kelly, who sounds like a moderate, but votes with Biden 94% of the time, have to go.