Can Markets Function Normally With Intrusive Central Planning?

Editors’ Note: On Friday, March 10, Silicon Valley Bank collapsed, the second largest bank failure in US history. There is common wisdom that the FED keeps raising rates “until something breaks.” There is likely no bigger single market intervention than the manipulation of interest rates. Along with the meltdown in cryptocurrencies, their banks, and exchanges, pension funds in the UK; this is the first really large banking failure. Officials in 2007-2008 suggested banking troubles were “isolated events”, but history proved later that was not correct. It will be very important to see how far the rot has spread in our financial system. Most all banks that own long-dated US Treasuries and mortgage-backed securities are taking large losses because of the FED sharply raising rates. These events illustrate the problem the FED must deal with. Having blown a huge financial bubble with cheap money, they must now deflate the bubble, but at the same time hope they can avoid the collateral damage that could plunge the economy into recession. If they back off too early, they lose the inflation fight. If they persist too long, they risk a recession. Trying to thread the policy needle just right represents a substantial risk to the financial markets.

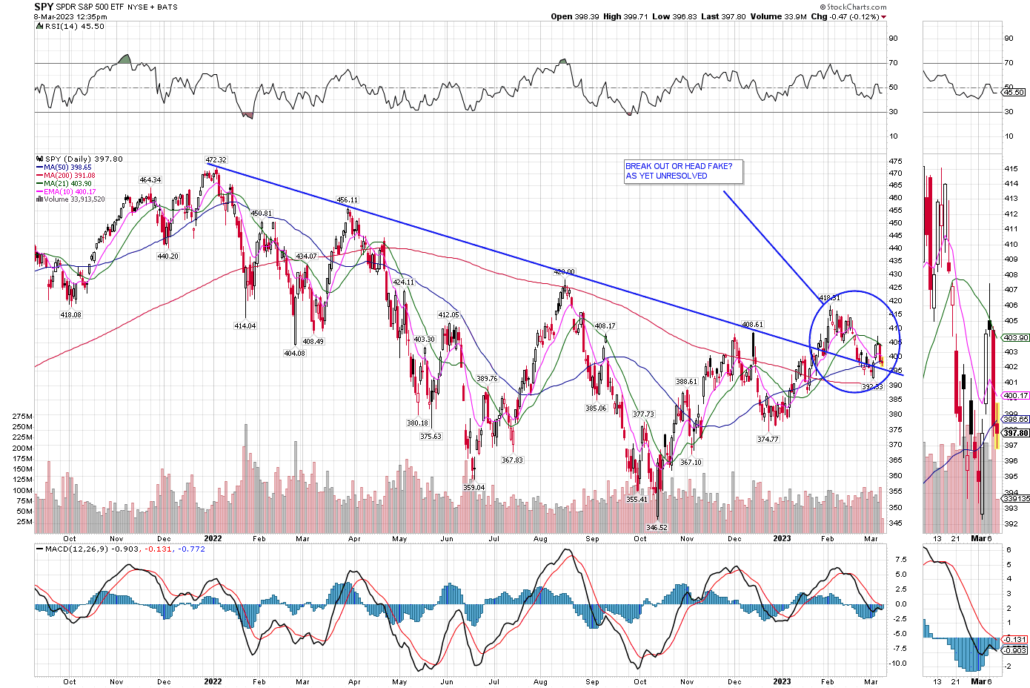

As readers may be aware of our past stock market commentaries, the stock market is at an important juncture. After last year’s bear market of a bit better than 20%, stocks started to rebound this year.

Historically, it is normal for the third year of a Presidential term to be bullish.

A rally from the worst of Covid-related economic trauma would also be expected.

The market seems to be going through a series of conflicting mental states: the economy will have a soft landing, the economy will have no landing at all, and recently, the economy will have a hard landing.

The recent rebound created internal strength and momentum sufficient that it has convinced a fair number of commentators, mostly of a technical stripe, that a new bull market in equities has begun. In their defense, the market did break its bear linear trend line and turn up major moving averages. It has a high number of “breadth thrusts”, high volume days where advancing issues swamp declining issues. So, it is indisputable that the market is acting better.

Curtesy of stockcharts.com

Oddly though, after the “break out” the market decided to confuse everyone even further by diving back to the breakout point and then fiddling around in narrow a range as we write. In part, this was because of Congressional testimony by FED Chairman Jerome Powell, who expressed a “higher for longer” position on interest rates.

Is it a new bull market or a bear market rally? Our best estimate has been that it is a bear market rally. Given the retreat back down to resistance we would have to say, the “break out” remains unresolved and thus a trend in force remains in force until proven otherwise. The trend in force has been a bearish downward trend.

We suggested this is a bear market rally based on the “weight of the evidence,” both fundamental and technical, although we frankly thought the market advance would last a bit longer than it did. Did Powell kill the baby in the crib?

The technical strength remains impressive. Even after more talk of higher interest rates, the market has refused to cave in. Instead, it fell right back to the resistance area, but so far has held…barely. However, it is fair to say that conditions are so fluid right now, it is probably best to avoid dogmatism.

For those of a more fundamental view, their concerns include the likelihood of a recession caused by rising interest rates, an inversion of interest rates, a decline in corporate earnings, a housing slump, a historic decline in the money supply, and increasingly stressed consumers. On the positive side, employment remains buoyant and unemployment is at very low levels.

It is also historically rare for a major bull market to begin with valuation levels still as high as they are. There has been a bear market for sure, but it is far short of the “average” bear market loss of 36% and given the credit excesses and valuation excesses of this Supercycle, it would seem a bit odd to end this affair with such a modest correction.

The technical analysts counter this with an important argument. The very nature of their system posits that all known factors are incorporated into the price structure. In other words, all the worries about recession and interest rates, and concerns about earnings and whatever, are known, and still, the market has decided it still wants to rise.

If we are all talking about these troublesome issues, they are known. If they are known, the market is already incorporating that in the price structure.

Since we use both technical and fundamental analysis in our own thinking, we do not have an ax to grind for either school of thought. Both are valid ways of making judgments about the market. Neither is perfect so the more supporting information you have, from either camp, the better your odds of making a correct decision.

The deeper question is whether either school of analysis can function well in an environment of heavy-handed central planning that is driven by a political agenda.

It has become obvious that some of the “data” that fundamentalists use are altered by government policy and the FED itself. Greater government benefits and societal changes have made it possible for something on the order of seven million men of prime age to disappear from the labor market. That does make the labor market look tighter than it otherwise would be.

Central planning supposedly involves a degree of secrecy, otherwise, those who know what policy shifts will occur can profit. However, it is amazing the number of congressmen and congresswomen, and even FED officials who have speculated on stocks given their privileged position to get inside information first. It would appear that ethics is no match for the self-interest of bureaucrats and politicians.

It can be argued that if that is the case, then the market does have information because buying or selling activity is occurring, spreading the information.

But how far must information be dispersed before markets get a true reading of demand? Nancy Pelosi herself should not be able to move markets, even if she and her husband may trade on inside information.

The theory of central planning also assumes there is a central plan. What if the FED simply makes things up as they go along, caves into political pressure, or is immersed in internal conflict that makes the mission less certain? The same can be said for the Biden Administration.

More frightening, what if they don’t know what they are doing yet are conducting a grand monetary experiment with Quantitative Easing, Quantitative Tightening, and Modern Monetary Theory?

We have never been in a situation where we are spending and borrowing on a scale of World War II, all in peacetime, and all on top of preexisting huge debt. There are scant historical examples to guide us through our current predicament. We are in a new historical territory almost every day.

You can readily see it is hard for markets to incorporate information into the price structure when there is little rhyme or reason to what central planners are doing. Improvisation of policy is difficult to discount unless you know what the whims of the prince will be. But if it was planned, it wouldn’t be a whim, would it?

Markets today may in fact be more like a gambling casino changing rules frequently based on the whim of the mob boss. If so, how well can markets discount future events and trends?

We do have markets today that jump around frequently not only the statements of officials in various venues, but also we have politically manufactured data that frequently get “revised.” Unless one has advance notice of what these spokesmen will be saying, it is pretty much a guess as to what they will be saying. The next guess is how will the market react to the latest statement.

Readers might recall the fall and winter of 2018 when the FED said they would raise interest rates. As soon as the markets began to correct, the FED immediately changed course. It was a monumental whipsaw for investors and under these circumstances, it seems difficult for markets to incorporate such fluid decision-making into the price structure.

Our point is that central planning today is more like planned chaos and is not often conducted either with consistent political or economic principles and is driven by pollsters.

Such conditions argue for intellectual modesty regarding a new direction for the market.

Finally, there is the problem central planning has always had. It relies little on market data and more on political whim. Because it does not rely on true supply and demand, central planning has never worked. You cannot make rational economic calculations absent true free market forces.

It is an open question as to how well markets can truly function in today’s era of central planning.

Markets must deal not with just what direction the economy may be going, but more often, with what direction intrusive government policy is going.

The FED is moving interest rates, the government is selling oil from the Strategic Petroleum Reserve, NATO is sanctioning Russian oil, government skews lending to diversity and equity, economic growth takes a back seat to environmental zealotry, and there is a general regulatory jihad against business in general. Recently, Treasury Secretary Yellen says she now believes “climate change” can alter the value of securities.

How good are our tools of analysis, technical and fundamental, under circumstances of constant and incessant interference by the government?

Probably not as good as we would like them to be.

Amidst all this, we accept the primacy of the dictum of “don’t fight the FED.” Right now, the markets seem like they want to fight the FED. Because of that, we prefer caution. Eventually, the markets will get a better sense of direction when we are closer to the end of this interest rate hiking cycle. We will find out if we indeed have had a breakout or a head fake.