Is This The Pause That Refreshes Or Something Worse?

When commenting on the stock market, it is difficult to establish continuity unless previous articles are referenced. We are sorry for that because it also requires the reader to go back to pick up the pieces of the argument.

Our point of reference is the last commentary written on August 3, 2023, wherein we suggested a number of market anomalies and mentioned the market was overbought looking “tired” after bullish opinion had hit very high and excessive levels. We wondered whether we were on the cusp of a market pause, that would work off short-term excess or the beginning of something worse to the downside.

We suggested using crawling stops, reducing exposure, and generally getting more conservative, especially for older investors or those that need or desire lower risk.

The market since early August seemed to have thankfully heeded our call so we don’t look terribly stupid at this point. The market has been feeble for three weeks and is on course for the worst August since 2001.

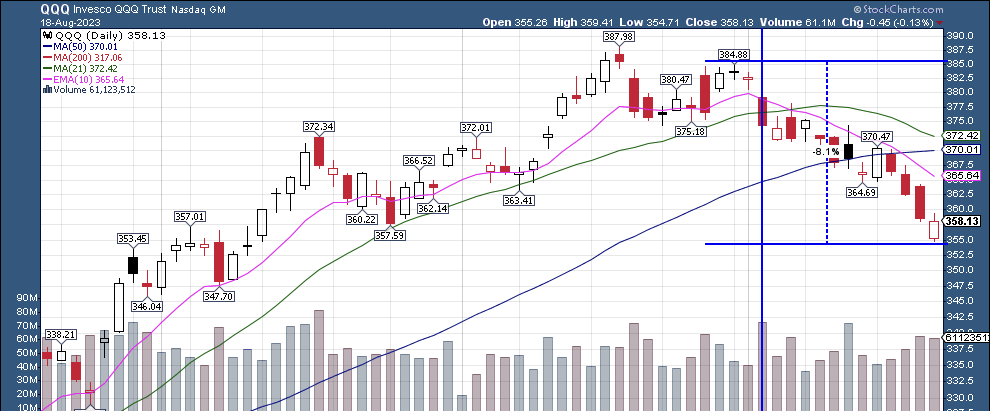

The chart above is of the QQQ, the top 100 stocks in the NASDAQ. The chart suggests the strongest part of the market is now in some difficulty. Although breadth did widen some, it was not enough to convince us. Now, even the strongest portion of the market appears to be losing momentum.

While the “magnificent seven” are up sharply on the year, the rest of the more than 490 companies in the S&P are down about 4%.

But, the market leadership has spent almost the entire month so far of August in decline and now will roll into September, the weakest month of the year in seasonality studies. So far, the losses of 8% are not that great, but they hurt nonetheless.

OK, we got lucky and got the short-term action correct, but now what?

The real question for investors is not whether our short-term call was correct rather it is whether this is the beginning of a “normal correction” that will work off some of the short-term excesses or is this simply the opening round of a much more protracted and larger decline?

The answer to our own question is we don’t know yet. So far, this just looks like one of the frequent declines investors usually experience in a “normal” bull market.

But the problem we are having is very few things right now are operating normally.

Yes, the stock market has had a good year so far, but because of the narrow breadth, it is misleading. When you have just seven stocks create something like 90% of the gains, in the S&P index, the world is going haywire.

People love index funds today and love ETFs. They buy “index funds” precisely because they don’t want to sector bet and because they want to be broadly diversified. But with a handful of companies providing such a high percentage of the gains, buying an index fund is long longer a diversified position! Indexing is no longer diversified investing, it is now momentum chasing a narrow selection of stocks.

This defeats the whole philosophy of indexing, which made it so popular and useful.

The market is unbalanced with such concentrated performance and suffers from severe “bad breadth.”

One of the tried and true rules (we would credit the late Martin Zweig) is “don’t fight the FED.” His admonition was not to expect good outcomes when the FED is raising rates. The auxiliary rule is also, don’t fight the market when it too is raising rates. The fact is rates have been heading aggressively higher in the recent term, and it is only in the last few weeks the market took a pause from its mania to notice.

The yield on the bellwether 10-year US Treasury now is at its highest level since 2007. Does anyone remember what followed in 2008-2009?

It is good to remember that rapid increases in interest rates usually have a lagged effect. Interest rates only pinch when the credit line or financing you are using must be renegotiated. Hence, the economic pain comes well after the increases have taken place.

The FED will have its Jackson Hole confab on August 24-26 and then will have its regular meeting on September 19-20. The market will likely be sensitive to all the “FED talk” that will emanate from these meetings, particularly if higher rates are once again discussed.

Many have labeled this a “new bull market” simply because of a 20% move. As we have stated before, there is more than that to the story. There have been about seven rallies of 20% or so that did not become “new bull markets.” Additionally, new bull markets usually begin from a condition of undervaluation. This market advance began from historically high levels, and the handful of market leaders launched from truly nosebleed levels of valuation.

While the economy is technically not in recession, the actual determination of “recession” is done well after the fact. That is not helpful to investors who would like to know beforehand. So watching the economy may not be an advance indicator that can give you prior notice of stock market behavior.

Having said that, for those using the economy for guidance, there are many areas of weakness in the economy and everything has been distorted by massive fiscal stimulus, which seems to be contradicting the FED’s monetary policy. Biden is stimulating, the FED is removing stimulus. Nevertheless, the leading economic indicators have been down now for about sixteen months.

The economy could at best be described as ragged but we don’t think it is strong.

As the economy came out of Covid Lockdown, of course, some sharp rebound would be expected. Add to that a huge dose of fiscal stimulus, and you have an economy that looks pretty good on the surface, but underneath looks quite anemic.

The market is now breaking down through some of the intermediate moving averages. That is pure price action. Price momentum to the upside has been at least temporarily exhausted and now downside action must be exhausted.

Our biggest worries continue to be the beating bonds are taking. The FED is a seller, Social Security is a seller, many foreign central banks are sellers, and the US Treasury is a huge seller to fund massive new deficits.

Lower bond prices mean higher interest rates in a world that is awash with debt, much of it of low quality. There is an increasing risk of some sort of credit incident that could rock the stock market for, at least a while. It could come from the domestic side or the international side. Our bones are telling us the highest rates in 22 years will take their toll on the over-leveraged borrower and we could well see another “Lehman” moment.

According to the Kobeissi Letter, it would appear that most of the stimulus cash pushed into the system over the past two years has been spent and the “sugar high” provided the economy may be ending.

As Stephanie Pomboy notes in the attached video, the impact of higher rates occurs when companies have to refinance debt that is maturing. Over the next three years, that amount will increase substantially, and that may be the cause of increased corporate bankruptcy filings. Her analysis of the corporate sector is important and worth your time, even if some of it sounds a bit arcane. The fact is the strength of corporate balance sheets is just as concentrated as the price performance of the stocks themselves.

Commercial real estate is looking quite stressed and rising rates are hitting the consumer, especially those that use credit cards to finance purchases. Interest on credit cards is now over 20%, having been at 14% just about a year ago. Delinquency rates on lower-quality automobile loans are rising sharply.

The affordability index for housing has just exceeded the 2007 peak, the level seen just before the last housing bust began. Between escalating mortgage payments and car payments, consumers must either wind down cash or take on even more credit.

We live in an integrated world economy. China is in recession and is showing signs of credit problems again, especially in its massive real estate sector. Germany, the largest economy in Europe is already in recession.

The large and serious market moves historically have an international component to them.

The one positive for investors is rising rates are increasingly making the yield on short-term bonds look favorable. We no longer live in a world where there are no alternatives for investors except stocks. Short-term US Treasuries and CDs now yield over 5.5 % and look to get even better.

Rising rates pressure home sales. The 30-year fixed rate mortgage is now almost 8%. The bulk of wealth in this country for the vast majority of people is in their homes. If home prices start to crack, they will feel less wealthy because they are less wealthy. If they then curtail consumption out of fear, the economy could weaken quickly.

To be fair, there are some good things about the economy. But that information is generally available in the standard media sources who want to tout how great things are under Biden. Therefore, it is likely you know elements of the good story (low unemployment, moderating inflation, a resilient consumer, the nirvana of a soft landing) but these same sources will not point out the ugly part of the story because it does not fit their narrative of Washington and Wall Street.

There are legitimate reasons to be concerned about narrow market breadth, sharply rising rates against an enormous debt bubble, the inverted yield curve, and the ragged action of the economy. You can’t raise interest rates at a record pace on an economy that has twice as much debt as it had in 2007 without consequences, at least at some point. The timing, as usual, will be difficult if not impossible to know. We hope this correction will be mild and short-lived, and hence will “refresh” the market. But a major “credit event” is likely and could make it much worse.

We still urge those who cannot afford the risk to play the game safely. There are many conflicting indicators and more than a few negative ones. It just makes sense to be cautious.