Mortgage Volume Gets Crushed by Spiking Interest Rates: What it Means for Future Home Sales and Consumer Spending

The boom is over. And there are broader effects.

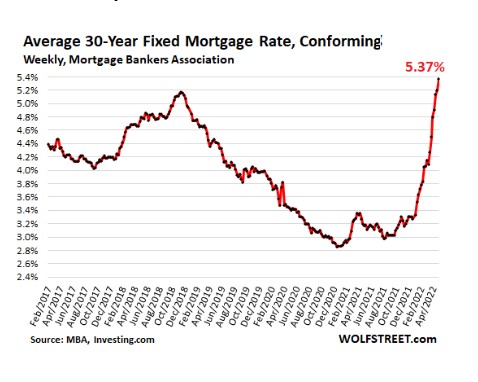

Spiking mortgage rates multiply the effects of exploding home prices on mortgage payments, and it has taken layer after layer of homebuyers out of the market for the past four months. And we can see that.

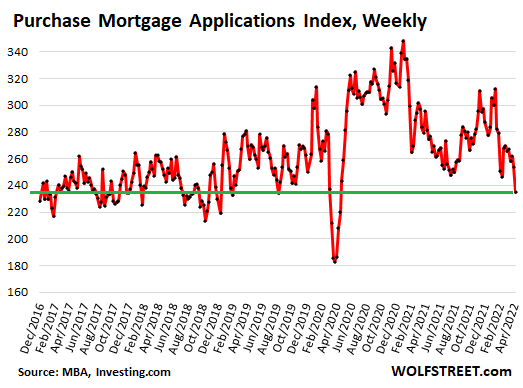

Mortgage applications to purchase a home fell further this week and were down 17% from a year ago, hitting the lowest level since May 2020, according to the Mortgage Bankers Association’s weekly Purchase Index today. The index is down over 30% from peak demand in late 2020 and early 2021, which was then followed by the historic price spikes last year.

“The drop in purchase applications was evident across all loan types,” the MBA’s report said. “Prospective homebuyers have pulled back this spring, as they continue to face limited options of homes for sale along with higher costs from increasing mortgage rates and prices. The recent decrease in purchase applications is an indication of potential weakness in home sales in the coming months.”

What this means for homebuyers, in dollars.

The mortgage on a home purchased a year ago at the median price (per National Association of Realtors) of $326,300, and financed with 20% down over 30 years, at the average rate at the time of 3.17%, came with a payment of 1,320 per month.

The mortgage on a home purchased today at the median price of $375,300, and financed with 20% down, at 5.37% comes with a payment of $1,990.

So today’s buyer, already strung out by rampant inflation in everything else, would have to come up with an extra $670 a month – that represents a 50% jump in mortgage payments – to buy the same house.

*****

Continue reading this article at Wolf Street.